Investment in agriculture

Download the pdf file: Agricultural_investment.pdf

Investment in agriculture1

Present investments shape the future. This is why, the analysis of investment in agriculture helps to figure out in which direction agriculture (and food) will evolve in the years to come.

Agricultural investment increased considerably over the last 25 years

At world level, investment in agriculture (including forestry and fishing), captured by gross fixed capital formation2, more than doubled between 1995 and 2019. This period of growing investment follows a spell of relatively stagnating investment amounts in the sector.

As indicated in the graph below (Fig.1), investment in agriculture accelerated after the middle of the first decade of the century, particularly after the 2007-08 food security crisis. Most of the increase observed originates from middle income countries, while it was minimal in rich countries. Investment in poor countries remained marginal.

Fig.1: Evolution of global agricultural investment (1995-2019)

Source: FAOSTAT

download graph: Investment_evolution.png

{kind=link}

With respectively a 4 and 3.4 times increase of their annual agricultural investment, India and China have been key contributors to this trend. As a result, more than half of agricultural investment is now made in rich countries and in China.

The disparity in agricultural investment per inhabitant is huge among country groups, amplifying future inequalities. Interestingly, while the share of agricultural GDP invested back into agriculture is around 16% worldwide, it is almost double (29%) in rich countries, and only 9% in Africa. This means that investment in agriculture per inhabitant is 14 times bigger in rich countries than in poor countries (Table 1). As a result, agriculture is much more capital intensive (and productive) in rich than in poor countries where agriculture relies mostly on labour, and the gap between the rich and the poor is likely to grow.

Table 1: Evolution of global agricultural investment per inhabitant (1995-2019)

(in US dollars/inhabitant)

Source: FAOSTAT

New driverless tractor (USA) Farmer ploughing (Myanmar)

Private investment

New, profit-oriented, operators have entered agricultural investment

Traditionally, the bulk of investment in agriculture had been made by farmers, followed by public organisations. In recent years, new players have taken more importance, as market integration of agriculture increased. Urbanisation encouraged the emergence of complex food and agricultural value chains that ensure the processing and movement of agricultural products from primary producers to consumers. This has profoundly transformed the global food and agricultural system during the last decades, and this trend is accelerating.

Large private companies, often multinational, funded by financial operators such as pension funds, specialized investment funds, endowment funds as well as impact investors3 and big data companies have joined more traditional private corporations, traders, public agencies and farmers.

These changes have been fast occurring in North America and Europe, and more recently in Asia, and they are expected to spread worldwide. For instance, the number of investment funds focusing on farmland and food production grew from 7 to 300 between 2004 and 2020 [read]. Research was particularly targeted by venture capital. Amounts invested can be considerable. For example, venture capital represented around $4.8 billion in the food and agriculture sector in 2020, almost doubling from 2019.

New actors often concentrate in domains such as farmland, private equity, and specific areas like venture capital, private debt or green bonds. It is probable that the share of these players will continue to grow in the future.

The consequence of the entry of these new operators is that an increasing portion of investments in food and agriculture are mainly driven by market returns (Fig.2).

This evolution is likely to create a disconnect between capital intensive, market-oriented commercial farms, on the one hand, and small farms with little surplus and limited investment capacity, on the other, with the possibility of public policies and investments geared towards commercial agricultural production and value chain promotion being incoherent with policies and investments aiming to reduce poverty and food insecurity [read].

Whereas this evolution may lead to believe that food and agriculture will become more professional and market-oriented, one can nevertheless fear that it will not put food systems in a position to face the challenge of climate change and conservation of natural resources [read].

Fig 2: Private investment landscape in food and agriculture

Source: World Bank Group, 2018

download diagramme: Sources.png

{kind=link}

Self-financing remains the main source of funds for poor farmers, as access to credit is constrained

By far, self-financing by farmers is the main source of agricultural investment. For small farmers, however, limited savings and difficult access to much needed credit usually constrain investment. Because of lack of collateral and clear property rights, smallholders generally depend on informal sources of credit such as savings groups or credit cooperatives. They also have to rely frequently on moneylenders and usurers who impose exorbitant interest rates and drastic reimbursement terms.

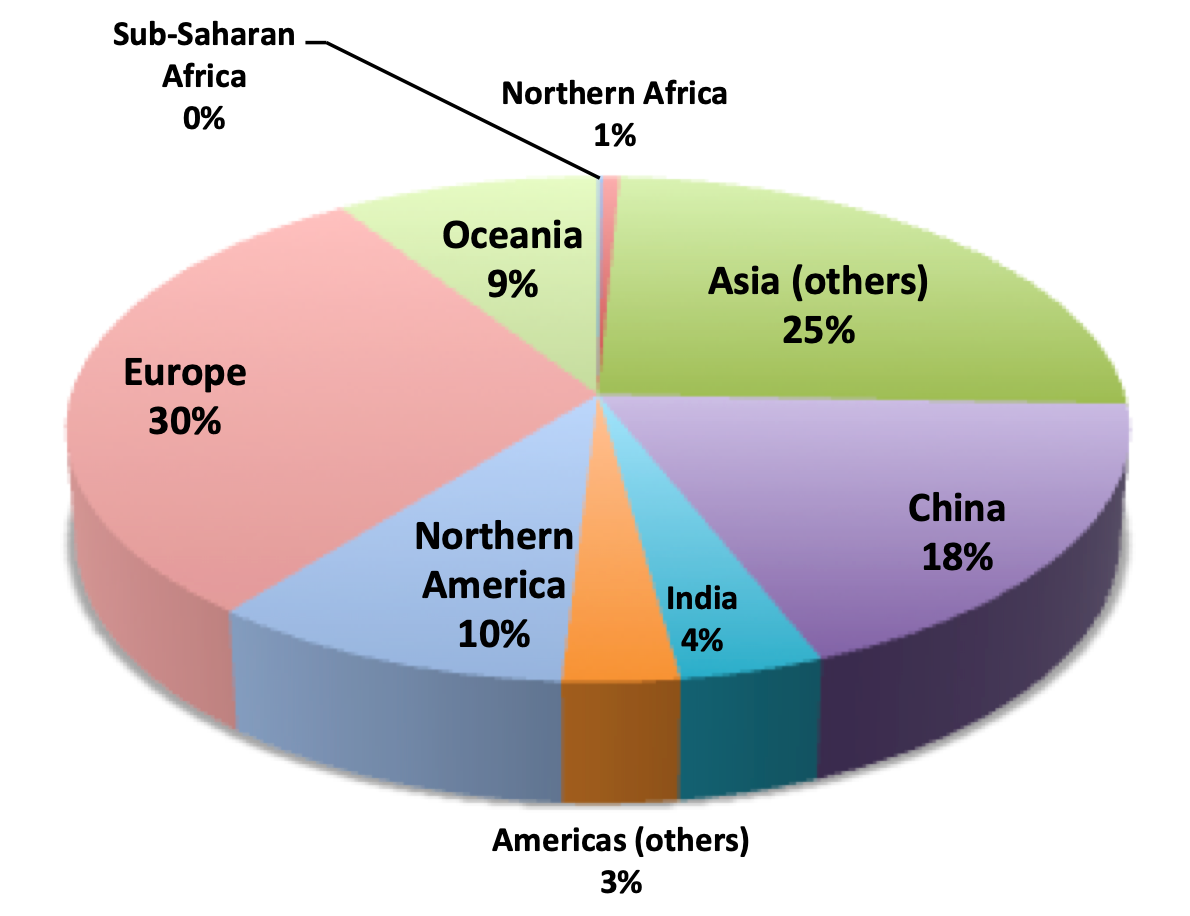

In fact, rich countries in Europe, North America and Oceania represented almost half of credit for agriculture, forestry and fishing worldwide in 2019, the rest being constituted mostly by Asia (47% of which 18% for China). In other parts of the world, agricultural credit is virtually non-existent (Fig.3). Here too, this situation is likely to lead to greater inequality and more exclusion.

Fig. 3: Distribution of available credit for agriculture, forestry and fishing in 2018

Source: FAOSTAT

download pie-chart: credit.png

{kind=link}

Small and medium enterprises face similar constraints in agri-food value chains, particularly in Africa

Like small farmers, small and medium enterprises dealing with food and agriculture are constrained by access to credit.

In Africa, nearly three quarters of these enterprises lack enough access to finance and the capacity to manage loans. The gap between capital supply and demand has been estimated at $65 billion a year [read]. Many small enterprises are not even banked and commercial banks generally find agriculture too risky a business to invest.

Foreign direct investment, often touted as the solution, remains relatively low in food and agriculture, compared to other sectors

A lot has been written on foreign direct investment. Some have acclaimed it as the solution for developing “developing countries” while others have criticized it as a way to increase domination of multinationals and rich countries.

In reality, it has remained relatively limited in food and agriculture, compared to other sectors, and was concentrated in food processing and services. It is mostly linked to export-related activities and driven by large multinationals [read]. It weighs 6% in total foreign direct investments in the area of food and beverages, and only 0.5% in agriculture, much less than in electronics or textile [read]. According to the UNCTAD, it has been multiplied fourfold in the food, beverage and tobacco industries during 2020 [read].

In agriculture, foreign direct investments have been linked to “land-grabbing” observed in the wake of the 2007-08 food crisis [read] and have been the object of controversies and criticisms. They have been associated with “non-consensual and uncompensated loss of land” by communities and “only little socio-economic benefits” such as “employments, productivity spillovers or infrastructure”. Negative consequences also included the destruction of “rainforests, natural habitats, and biodiversity” [read].

Public expenditure and investment for agriculture

There is clear evidence for governments to invest in agriculture in order to provide indispensable public goods and incentives through subsidies or grants to the private sector to invest in priority areas [read]. This notwithstanding, agriculture has been long neglected and public investment in food and agriculture has declined over time [read]. This is illustrated by the decrease of the share of public expenditure for agriculture in total public expenditure from around 7% to 4% between 1980 and 2007 [read].

Generally, public expenditure is taken as a proxy for public investment, although it also includes recurrent expenditure. This is particularly the case as it is not so easy to make a clear distinction between investment and other expenditures. However, depending on the country, the relative proportion of investment and recurrent expenditure in public spending on agriculture can vary considerably [read].

Agriculture: a neglected sector

The importance given to agriculture can be measured by comparing the share of agriculture in public expenditure to its weight in the economy. If this indicator, the Agriculture Orientation Index, is greater than 1, the government “overspends” on agriculture. If it is less than 1, it is “underspending”. In most countries, there is an underspending. In this sense, it is possible to speak of agriculture as being a neglected sector. Fig. 4 shows how this indicator evolved between 2001 and 2019.

At global level, the Orientation index has remained relatively stable over the period considered, oscillating between 0.4 and 0.5, indicating that the portion of expenditure used for agriculture in total public spendings is about half of the share of agriculture in the economy. It is worth noticing that no region in the world has been overspending in agriculture between 2001 and 2019, apart from North America in 2001. Mostly, agricultural spending has weighed in public expenditure less than half of its importance in the economy.

Asia has seen a consistent increase of relative spending on agriculture, reflecting the attention given to this sector by China, while Africa has clearly underspent on agriculture.

Fig. 4: Evolution of the Agricultural Orientation Index (2001-2019)

Source: FAOSTAT

download graph: AOI.jpg

{kind=link}

When considering this indicator at country level, the contrast is striking between, for instance, Nigeria and China. In the former, the value of the Agricultural orientation index is always less than 0.2 over the period - illustrating neglect -, while for the latter, it evolves between 0.6 and 1.3, demonstrating sustained attention!

The contrast between Asia and the rest of the world

Table 2 gives the level of public spending for agriculture per inhabitant and the share of agriculture in total public expenditure in 2016. It shows that the East Asia & the Pacific region was where public expenditure in agriculture per inhabitant was highest, mainly because it increased almost fivefold in China between 2005 and 2016 to reach close to $200 per person and per year (measured in constant 2011 US dollars). It is also the region where it represents the highest share in public spending. Public spending in agriculture has grown nearly everywhere in the world over this period, but in high-income countries. In high-income European countries, this expenditure was actually cut by half.

Table 2: Public agricultural expenditure in 2016 (in constant 2011 US dollars)

Source: IFPRI SPEED 2019

Meanwhile, in Africa, the share of agriculture in public expenditure remained at 2.2%, far below the commitment made by governments in 2003 to bring it to 10%. Actually, only a few countries managed to meet that target.

Fig. 5 shows that public expenditure in food and agriculture in the 13 African countries analysed by FAO’s MAFAP project was mostly for producer transfers (predominantly agricultural input subsidies), research & development and extension, agricultural infrastructure (primarily irrigation) and for transfer to consumers (through social protection programmes like cash transfers and school feeding) [read].

Strangely enough, although agriculture research has a high potential for returns (studies provided evidence of a 42% average rate of return [read]) and enhances farm productivity and household income, its importance has been dwindling in the countries analysed by MAFAP.

Fig. 5: Trends of public expenditure shares on food and agriculture

in MAFAP countries (2004-2018)

Source: FAO

download diagramme: MAFAP_diagramme.png

{kind=link}

In contrast, rich countries, China, India, Brazil and other middle-income countries have been investing in research (Fig.6), mostly by the private sector that is now leading research and orienting it towards the production of marketable goods and services often inaccessible to the mass of small farmers.

Fig. 6: Agricultural research spending by income group (1981–2016)

Source: ASTI

download diagramme: ASTI.png

{kind=link}

These circumstances question whether the orientation of research is likely to make production techniques evolve to make them more climate-friendly and able to preserve natural resources.

Foreign aid

Financial and technical assistance provided by foreign countries and international organizations can be a major lever for influencing changes in economies. Since 2002, Official Development Assistance (ODA) allocated towards agriculture, forestry and fishing has risen by over 156% to reach $10.2 billion in 2018 (Fig.7). It then amounted to 5.2% of total ODA [read].

Asia and Africa are the main recipients, but the importance of the volume of foreign aid to agriculture remains limited [read]. For example, in Africa for 2018, the $4.5 billion received represented less than 1.3% of Africa’s agricultural GDP, but almost three times national government spendings on agriculture, illustrating aid’s power of influence, as it generally comes with conditions and is attached to agreements between donors and recipient governments on policies, strategies and programmes to be implemented.

Of recent, in Africa, this influence has led to the adoption of strategies relying heavily on the leveraging of private finance [read], funded by blended finance [read] through which public resources support investments by private firms (often originating from the donor country). This orientation has tended to favour export-oriented activities and so-called hard sectors (infrastructure, banking and financial services) in middle-income countries, to the detriment of poorer countries and investments geared towards the eradication of poverty and hunger [read].

Fig.7. Total ODA for agriculture by all official donors (2002-2018)

Source: Ceres2030

download diagramme: ODA.png

{kind=link}

Conclusion

This brief analysis of global agricultural investment takes stock of great disparities existing in this area:

-

•While middle-income countries increased their agricultural investments, poor countries have seen theirs stagnating at a very low level.

-

•Private investment has seen new operators appear whose main objective is to make quick profits.

-

•Private investments are often made in the framework of value chains, and most foreign private investments are inked to exports.

-

•Small farmers and small and medium enterprises in poor countries have huge difficulties in getting access to credit, the bulk of which, at world level, is concentrated in rich countries and in Asian middle-income countries.

-

•Agriculture is generally neglected in public expenditure, particularly in Africa.

-

•Investments in Research & Development are being made mostly in rich and middle-income countries, and they are increasingly in the hand of the private sector.

-

•Official Development Assistance is a powerful tool of influence on policies, strategies and programmes being implemented in poor countries, especially in Africa.

From these characteristics of investment in agriculture, it is possible to infer that:

-

•although the gap among rich and certain middle-income countries seems to decrease in terms of investment in agriculture, it is growing with poor countries;

-

•the control by rich countries and some middle-income countries and their private companies on Research & Development carries the risk of further amplifying the technological gap and dependence of poor countries, and of leading towards even greater homogenisation of techniques rather than in favour of the development of production technologies adapted to local conditions and relying on natural biological processes [read];

-

•within countries themselves, disparities are increasing and the risk of marginalisation of the weakest producers and operators is growing;

-

•it can be reasonably expected that the greater professionalisation of agriculture and its increased reliance on the market, bodes ill for the future capacity of food systems to face the challenge of climate and conservation of natural resources.

(January 2022)

-----------------

Notes:

-

1.This document updates aspects of “Insufficient support to agricultural development”, published in 2013, and complements ”Public support to agriculture…” published in 2021.

-

2.Gross fixed capital formation (GFCF) is measured by the total value of a producer’s acquisitions, less disposals, of fixed assets during the accounting period plus certain specified expenditure on services that adds to the value of non-produced assets (FAO).

-

3.Impact investors are investors adopting approaches such as Socially Responsible Investing (SRI) and Environmental, Social & Governance (ESG) Investing [read].

——————————

To know more:

-

•UNCTAD, Global FDI flows down 42% in 2020 , Investment Trends Monitor, 2021.

-

•Pernechele, V., Fontes, F., Baborska, R., Nkuingoua, J., Pan, X. & Tuyishime, C., Public expenditure on food and agriculture in sub-Saharan Africa: trends, challenges and priorities. Rome, FAO, 2021.

-

•Land Matrix, Few development benefits, many human and environmental risks: Taking stock of the global land rush, Analytical Report III, Land Matrix, 2021.

-

•Attridge, S. and Engen, L., Blended finance in the poorest countries: The need for a better approach. ODI Report, Overseas Development Institute (ODI), London, 2019.

-

•World Bank Group, Future of Food - Maximizing Finance for Development in Agricultural Value Chains, 2018.

-

•Syed S. and M.Miyazako, Promoting investment in agriculture for increased production and productivity, FAO, Rome, 2013.

Selection of past articles on hungerexplained.org related to the topic:

-

•Responsible businesses or greenwashing? The certification industry in support of multinationals, 2021.

-

•Privatisation of development assistance: integrating further agriculture into the world market, 2018.

-

•Official Development Assistance, a drop in an ocean of needs, 2018.

-

•Opinions: Big Business Capturing UN SDG Agenda? by Jomo Kwame Sundaram and Anis Chowdhury, 2018.

as well as articles published under “Investment”.

Last update: January 2022

For your comments and reactions: hungerexpl@gmail.com